3 Oil Stocks To Buy, Whatever Oil Prices Do

These three companies should serve you well no matter what

These three companies should serve you well no matter what

Oil stocks have looked more lively recently. U.S. crude oil is up 25.85% year to date, with West Texas Intermediate (WTI) recently trading around $57.15 a barrel. That comes as the Organization of Petroleum Exporting Countries (plus non-members including Russia) holds one of its regular meetings at its headquarters in Vienna, Austria. It has committed to extending the agreed cutbacks in production of 1.2 million barrels per day (MBPD).

And then we have various conflicts in the Middle East, which makes U.S. (particularly Texan) and North American production that much more important to global oil supplies. WTI is also moving in sync with Brent Crude spot prices, which recently traded at $63.27 a barrel, as shown in the graph below:

WTI Spot (CL1) vs Brent Spot (CO1) (Source: Bloomberg)

Now, this is really good for oil exploration and production (E&P) companies. But for a more defensive means of investing in oil — whether it be rallies higher or subsides — I recommend that we go to the midstream pipelines.

Pipelines have less exposure to the ups and downs in the price of oil. However, they do benefit from demand — the higher the demand, the more oil that flows through the pipes.

I’m seeing further evidence that that’s exactly what we should see for a while, given the market conditions.

Put ‘Er There Partner

Now, the stocks that I’m recommending aren’t just common stocks but partnerships as passthrough securities. Passthroughs get their name from how they pass on their dividends to shareholders. Investors get their cut of the majority of the operating profits directly passed through to them in the form of checks or credits in their brokerage accounts. These checks do not get taxed at the company level thanks to Ronald Reagan and his signing of the Tax Reform Act of 1986.

With those checks, unit holders also get a cut of all of the tax deductions and credits, including depreciation, depletion and other bits that effectively shields much of the checks from current-year income tax liabilities.

This makes these checks even more valuable on an after-tax basis.

But there are a couple of drawbacks and one additional benefit.

The first drawback is that for each bit of each check that gets a tax benefit, the unitholder’s cost basis in the units gets reduced. So, if and when the unit holder sells the units, then they will pay capital gains taxes if the units are priced higher than the adjusted cost basis.

And the second drawback is that unit holders need to hold their units in a taxable account and not an IRA. This is also because of the Tax Reform Act of 1986. Because unit holder income isn’t taxed regularly like stock in a regular company, the act sets up a particular rule.

If tax-shielded investments such as passthroughs are held in an IRA and the net taxable dividends in an account exceeds $1,000 in a specific tax year, then that income would become taxable under the IRS Unrelated Business Taxable Income (UBTI) rules. So, to avoid having non-taxable dividend checks from passthrough units becoming taxable, it’s best to have them held in regular taxable accounts.

But there is one additional benefit to these oil stocks. If you don’t sell your units before your death, then your estate will inherit your units and the cost basis gets reset to the then-current value. That means your beneficiaries will not owe one dime in income taxes on the units. (Of course, there’s still the death tax, but that’s another matter.)

In Oil Stocks, The Pipes are Calling

Pipeline units are very attractive generators of dividend checks.

Passthrough pipeline units were widely sold off after the Tax Cut & Jobs Act (TCJA), as some feared that the attraction of lower general corporate tax rates would draw institutional investors away.

But for us individual investors, the tax-shielded dividends remain very attractive because the TCJA did nothing to reverse the great parts of Reagan’s 1986 tax deal.

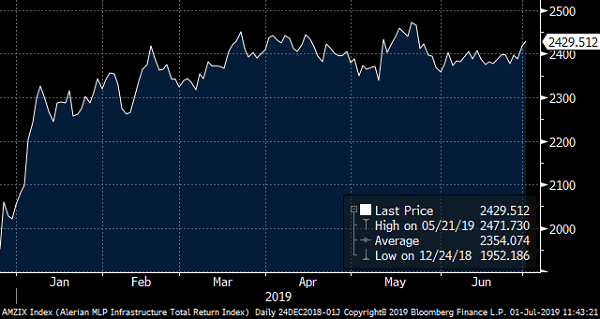

Pipeline Partners Pounce! (Source: Bloomberg)

Folks are now catching on to this. As a result, the market for pipeline units has been climbing since last December, as you can see in the Alerian Infrastructure Total Return Index above.

Oil Stocks to Buy: Plains GP Holdings (PAGP)

Right now, if you want to focus on the crude pipes, buy first into units of Plains GP Holdings (NYSE:PAGP).

Plains owns general partnership (GP) interests in Plains All American Pipelines (NYSE:PAA), which has oil gathering and storage facilities as well as pipeline and other transportation structures around North America. The transportation unit moves nearly 5 million barrels per day of crude and natural gas liquids

Its customers are a who’s who in the oil market, including Marathon Petroleum(NYSE:MPC), ExxonMobil (NYSE:XOM), Phillips 66 (NYSE:PSX) and others.

Revenues are up over the past year by some 29.9%, and while operating margins are a little thin at 6.7%, remember that the company moves a lot of petroleum.

Plains GP Holdings (PAGP, Source: Bloomberg)

The company has little debt compared to its vast assets and pays out the majority of its profits, as it must under tax law, to unit holders. The dividend check payouts yield 5.7%, and all of the unit checks payouts are completely shielded.

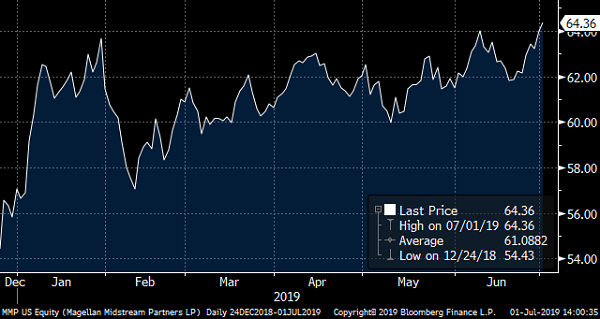

Oil Stocks to Buy: Magellan Midstream Partners (MMP)

The next units to buy into are in Magellan Midstream Partners (NYSE:MMP). Magellan runs a massive network of assets to store, transport and distribute petroleum and related products. These range from crude oil to refined products. It has a network of 12,000 miles of pipe and 50 terminals to gather and transport its contracted liquids. And for storage, it has the ability to store 85 million barrels of petroleum liquids.

The company’s up- and downstream customers include Shell (NYSE:RDS.A, NYSE:RDS.B), Kinder Morgan (NYSE:KMI) and Marathon Petroleum.

It is well structured to transport domestic products as well as to provide marine transport access for imported and exported petroleum — ever more important with the U.S. now being the largest producing nation on the planet.

Revenues are up over the trailing year by 12.7%. And for its crude oil businesses, revenues continue to surge on average by 14.2% over the past three years alone. Operating margins are very high — particularly for a midstream company — at 36.5%, which drives an impressive return on shareholder’s equity of 56%.

It has ample cash on hand and debts are a bit more than some of its peers at 55.1% of assets, but with ample cashflows and margins it’s not too big a worry. The quarterly dividend distribution is running at $1.005 for a current yield over 6% and is projected to be raised again this year. The MMP stock dividend has risen for the past five years alone at an average annual rate of 11.47%.

Magellan Midstream Partners LP (Source: Bloomberg)

It is a bit more expensive, with a price-to-book ratio sitting at 5.6x. But the underlying actual book value is up nicely from last year. And so far for 2019, shareholders have enjoyed a return of 16%.

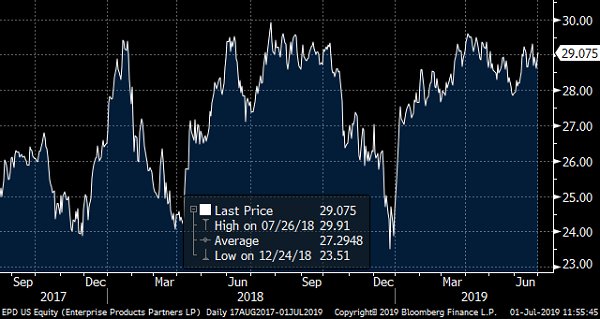

Oil Stocks to Buy: Enterprise Product Partners LP (EPD)

And the third units to buy into are in Enterprise Product Partners LP (NYSE:EPD). Enterprise Product Partners is a Limited Partnership, with unit holders having interests in four businesses.

The first is the crude oil pipelines, which bring in about 30% of revenue from 5,400 miles of pipe as well as storage facilities and marine terminals and also has an oil market company.

At its core is the strategic Seaway Pipeline that connects the U.S. oil hub in Cushing, Oklahoma, with the markets in Texas and beyond.

Second is the natural gas liquids business, with processing plants, pipelines and storage facilities. It generates about 45% of revenues for unit holders.

Third is the refined products and chemicals business. It processes petroleum chemicals and transports the goods to a host of manufacturers and refiners. It generates about 15% of revenue for unit holders.

Fourth are the natural gas pipelines, with 19,000 miles of pipe in the core gas markets of Texas and Louisiana.

Enterprise Product Partners LP (Source: Bloomberg)

Revenues are up over the past year by 24.9%. And margins are great at 13.5%. Like the other partnerships, debt is low compared to its assets at a level of 46.2%.

Units are priced a bit more at 2.6x the net book value of the partnership’s assets, and the unit holder’s dividend yield sits around 6%.

Neil George is the editor of Profitable Investing and does not have any holdings in the securities mentioned above.

See Also From InvestorPlace:

- 7 A-Rated Stocks to Buy for the Rest of 2019

- 5 Dividend Stocks to Buy From Across the Globe

- 7 of the Best SPDR ETFs — Besides SPY and GLD

Category: Commodity Stocks