Is Buffett Wrong About Gold?

Image by Unsplash

If you asked 100 random people today who in their opinion is the most known investor, probably 70 would mention Warren Buffet, the icon of investing in stocks. The legend that has been built around the “Oracle of Omaha” over the last 40 years is indeed impressive.

While I very often agree with his views regarding, for example, the level of cash in portfolio or migration from growth to value stocks, I absolutely can not agree with what he wrote in the letter to shareholders about gold, once again showing how badly it performs in comparison to the US shares.

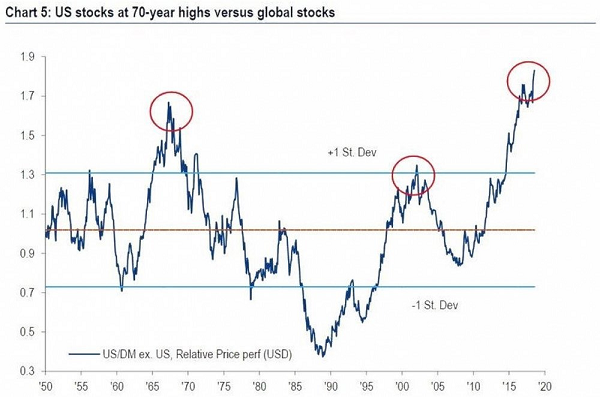

I do not want to question Buffet’s knowledge at any point, but after reading his views, one conclusion comes to mind: “sell gold and buy American stocks.” Buffet is an icon, legend and nothing will change that. The fact is, however, that the past decade has greatly improved his results. Over the past 10 years, global speculative capital has been flowing strongly to the US, as a result of which shares on the NYSE are the most overvalued in relation to other markets since the research has began.

Source: BofA Merill Lynch

What is the probability that such a level will last for a long time? Close to zero. In order to show you how owning such overvalued one asset class in a portfolio ends, I will show you the results of Buffett’s strategy during several periods that the management of Berkshire Hathaway would probably like to forget.

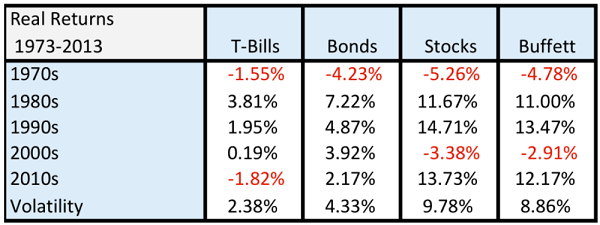

For this purpose, I used the data from the analysis of Meb Faber (not to be confused with Marc), called Global Asset Alocation. For the sake of clarity, Buffett’s strategy is based on investing roughly 90% of capital in US equities. It is not surprising that it works well when the prices of NYSE stocks growing strongly. What if stock prices are not changing or falling?

Source: Meb Faber, Global Asset Allocation

Let’s see:

In 1973 (beginning of research) – 1980, Buffett’s strategy suffered real losses (after taking inflation into account) in the amount of 4.78% per annum for 7 consecutive years, reaching a cumulative loss of 38.6%… a lot.

Why did this happen? First of all, the starting point of the analysis was the time when stocks in the US were expensive. They were no longer in the extreme bubble phase like 4 years before, but the valuations were still at a very high level. If we would analyze the period from 1969 (the bubble’s peak), the investment loss based on Buffett’s strategy would reach 60%.

The following years are a period of very good results. First, because in 1981, the US stock exchange had been extremely cheap. Secondly, because in the next decade (1990-2000), capital from Japan (after the bubble had burst there) had moved to the USA. Ultimately, two decades of decent growth had ended in a bubble on technology stocks.

The story, as you know, likes to repeat itself and the years after 2000 have not been good for Buffett’s strategy for the same reason as three decades earlier. Very high valuations!!! Well, owning US shares for the first decade of the 21st century has generated a real loss of 2.91% per annum. Apparently it is low, but the compound interest for 10 years has made its job. We can not forget that in 2008, a significant part of the companies of the Buffet’s portfolio had been given 800 billion dollars of non-returnable assistance at the expense of taxpayers in the form of TARP without which many companies would have disappeared from the market.

Therefore, does it make sense to stick to the US stock market only?

Absolutely not, especially nowadays. First of all, because of the volatility, which is higher when the concentration of one asset class in our portfolio is bigger, by owning 90% of US shares in our portfolio, we risk losing almost 50% of our capital in just one year (max drawdown). How many of us after such a big loss would be willing to buy cheap stocks? Hardly anyone. Such a big loss will mentally exhaust many people. What is even worse, if knowledge and common sense prevail in some of us to buy these cheap stocks, we still only have 10% of the capital that we have kept in cash for special occasions.

Source: Meb Faber, Global Asset Allocation

It is worth noting in the case of some portfolios, such as Permanent (described several times on the blog) or Marc Faber’s portfolio, the declines have been much smaller, which we owe to diversification into assets inversely correlated with shares.

What I absolutely want to emphasize is the fact that the 1970s belonged to commodities and precious metals, not shares. As you can see below, virtually all portfolios based on shares or bonds have been hurt heavily. The model based on the Buffett strategy has lost an average of 3.5% annually, 60/40 (stocks / bonds) over 4%. Bonds has lost the most – over 5%, as a result of drastic increase in inflation and interest rates.

Source: Meb Faber, Global Asset Allocation

Two portfolios that have generated a profit above inflation are: Faber – investing 25% of capital in gold or platinum and 25% in real estate or REITs and also a classic Permanent portfolio.

Why do I draw your attention to it?

a) Well, over the past decade, central banks have printed enormous amount of the currency, just like the US in the 1960s, to finance expenses related to the construction of “Great Society” and the war in Vietnam.

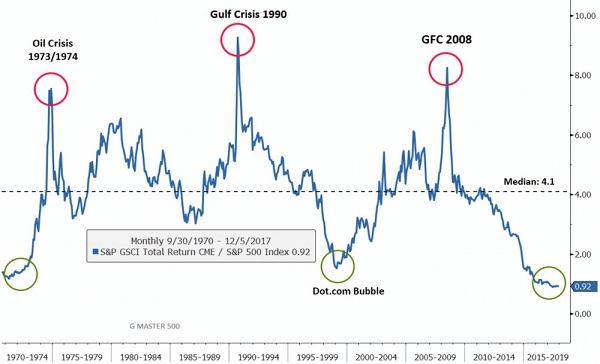

b) At the beginning of the 1970s, we also had very undervalued commodities (below you can see their comparison against stocks).

Source: Bloomberg, Incrementum AG

c) Sixteen-year dollar cycles suggest declines of the main reserve currency over the next years. The exception will probably be a period of several months of panic on the markets. This is important because the weak dollar translates into commodity prices increases and worse results of the US stock exchange.

Source: stockharts.com

d) Finally, come back to the chart from the beginning of the article and look what has happened to the US stock market after it reached a similar level of overvaluation (1969) as it is now. Draw the conclusions by yourselves.

Buffett’s investments and his strategy are two completely different things.

Describing the typical Buffet model, 90% of the capital invested in US shares is quoted through the cheapest ETF and 10% is in cash or short-term bonds kept for special occasions. Meanwhile, Buffet, and basically headed by him, Berkshire Hathaway invests in a completely different way. Being at the conference last year, I talked to a friend who regularly interviews Buffet. At that time, the share of cash was at 39%, as far as I remember. This was related on the one hand to high valuations and on the other hand to a very high level of optimism. In this environment, partial removal of capital from the stock market makes the most sense.

Buffet does not invest in broad market but instead selects the sectors carefully. Currently, due to the huge overvaluation of growth stocks (like Tesla or Netflix) in comparison to the value stocks (Coca Cola or BP), a significant part of the capital is invested in defensive companies that perform fairly well during the bear market.

Source: Thomson Reuters Datastream

At last, a very important difference between the actions of the legend and the strategy attributed to it is the fact that he is the insider with particularly good access to information and politicians, which greatly encourages investment in both shares of individual companies and acquisitions of them.

Summary

I really respect Buffett’s approach to investment. His results, especially in the last decade, are very good, but his portfolio is too dependent on the US stock exchange, which has been demonstrated by 48% decreases after Lehman’s bankruptcy, and in that time, shares in the US have not been as overvalued as it is now.

In my opinion, Buffet’s mistake is bypassing both commodities despite their strong undervaluation and precious metals, which he stigmatizes in public statements. I do not really understand why he does not talk about commodities, but negative statements about gold are most likely a part of a deal with the establishment of the United States. Buffet is the part of a dollar based system and its global supremacy. He has been the great beneficiary of TARP in 2008 and probably must somehow pay off debts to maintain a good relationship with the people who control the system.

Note: This article appeared at ValueWalk.com. It was contributed by Independent Trader.

Category: Gold